- The largest sunflower oil producer, with 7% of global production and responsible for 15% of global exports

- Price-to-earnings under 4, and it is trading at 2.8x free cash flow with clear competitive advantages in the industry, and fully integrated operations

- Ukrainian land reform gives Kernel the ability to acquire land and opens the door for further legislation

- Chairman of the board and founder owns ~39.2%

- Constraints in exports in Russia and Ukraine could push sunflower oil prices higher

- Considerable risk of a full-fledged conflict between Russia and Ukraine is a major risk and explains why the shares are so undervalued

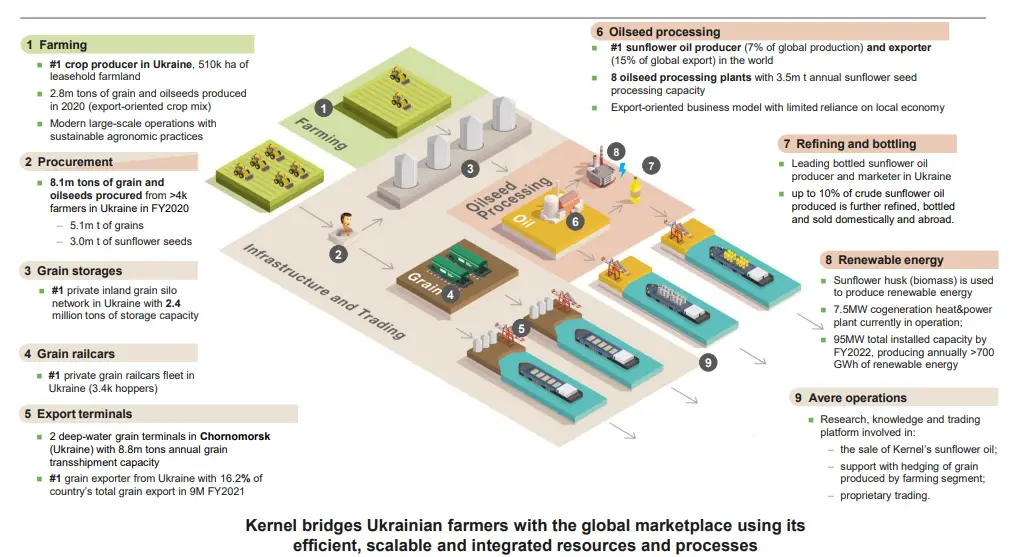

Kernel Holding, S.A. (WSE: KER) is the largest sunflower oil producer and exporter in the world, and it is located in Ukraine. It represents 7% of the global production and 15% of the exports. Its operations are well integrated vertically and it controls every step of the process. From laying the seeds on the ground to bottling and distribution. It is also involved in commodity trading and has considerable hedging ability given its large production.

Kernel overview

Recent constraints in exports from Russia and Ukraine will also limit global exports of sunflower oil and could contribute to higher prices. Ukrainian law does not allow companies to own farmland outright, and the law will be reversed in 2024. This can be materially beneficial to Kernel, which is the largest crop producer in the country and holds the most leases on farmland.

The Chairman of the board and founder owns ~39.2%, and its interests seem to be aligned with shareholders. Considering all the tailwinds, the dirt-cheap valuation at under 3x free cash flow, and a price-to-earnings under 4, we see tremendous potential for Kernel Holding. Even if we take in consideration the risks associated with investing in Ukraine and a potential full-fledged conflict between Russia and Ukraine

Despite the risks and given the fact that inflation is gaining some momentum, we think Kernel has a great risk/reward profile.

Source: Investor Presentation

Source: Investor Presentation

Kernel is the sunflower oil market leader

The global sunflower oil market is currently estimated to be worth ~$16.3B and it is expected to grow to ~$19.69B by 2027. A modest CAGR of 3.2%. Sunflower oil prices have seen a steep increase over the last year, and into 2021. Aided in part by the recent inflation fear.

Source: FRED

Source: FRED

Russia and Ukraine are the largest producers worldwide. The global production of sunflowers is roughly 47.347M tonnes per year. Ukraine is responsible for producing 13.626M tonnes each year. Therefore Ukraine is responsible for approximately 29% of the global output of sunflowers. Russia on the other hand controls ~23.3% of the global production. Combined, both countries control ~52.3% of the global sunflower oil output. This is particularly important given that both countries have been taking measures to reduce the impact of rising prices.

In Ukraine, sunflower crops declined by 15% during the 2020/21 season, and this has also contributed to higher prices. The Ukrainian government decided to act, and along with a consortium of sunflower oil producers in the region, is capping exports at 5.38M tonnes for 2021. This represents a decrease of ~19.5% when compared with the previous season. Russia is choosing a different route, but the objectives are the same. It increased the duty on sunflower seed exports to 50%, from 30%. With a minimum tax of $320/tonne. Taking into account that both countries represent over 50% of the global output, and are taking measures to tighten global supply - sunflower oil prices will certainly continue to increase.

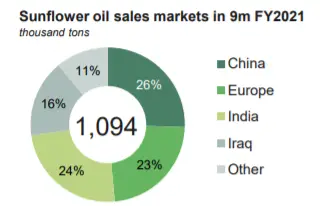

Despite the tighter export policy, Kernel exported ~1.094M tons of sunflower oil in 2020/2021, and given its pricing ability it should have no problem maintaining the same export volume in 2021.

Kernel Holding segments

Kernel has three major segments: Oilseed Processing, Infrastructure and Trading, and Farming.

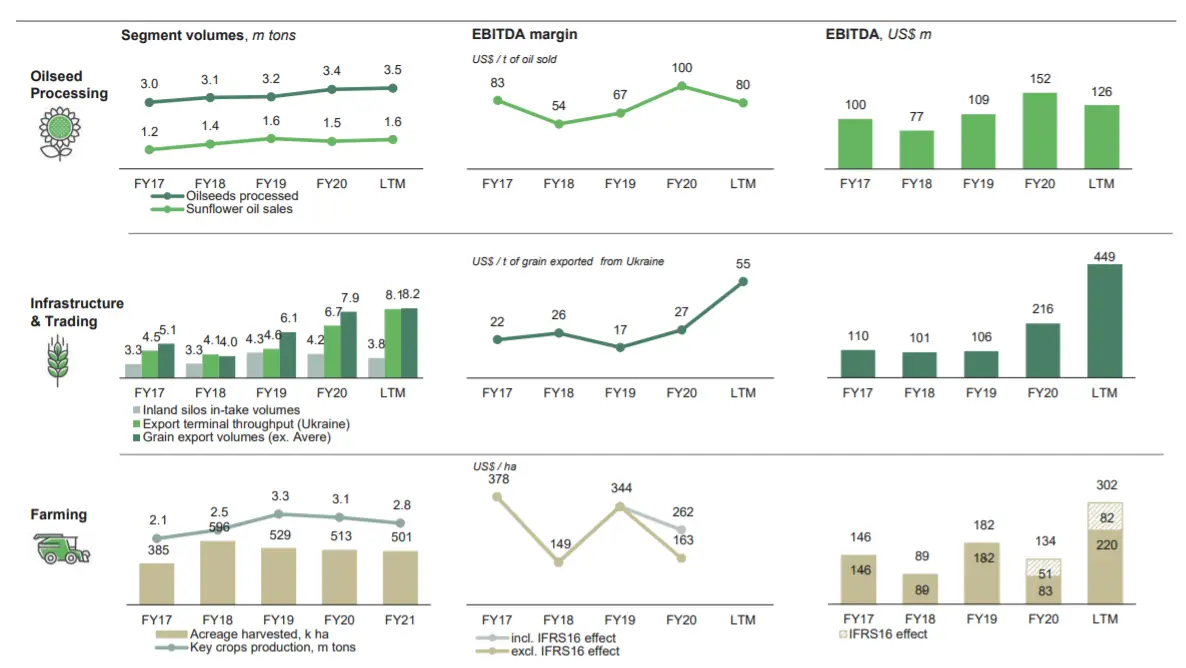

Its Oilseed Processing segment comprises 8 processing plants located across Ukraine. With the ability to process up to 3.5M tons a year. Every year ~47.347M tons of sunflower are produced, so Kernel in essence has the ability to process ~7.4% of the global production. For FY20, the oilseed processing segment generated ~$152M in EBITDA. Most of Kernel’s sunflower oil exports end up in China, Europe, India, and Iraq. They make up 89% of Kernel’s exports.

Source: Investor Presentation

Source: Investor Presentation

Infrastructure and trading is the fastest-growing segment. EBITDA for the segment grew 107% to ~$449M LTM when compared with FY20 results. Kernel is the largest grain exporter in Ukraine, representing 16.2% of the country’s total grain exports. It has the largest silo network in the country, with a storage capacity of 2.4M tons. Kernel also owns Avere, a subsidiary engaged in the trading of grains that helps the company hedge its large production.

Kernel is the largest crop producer in Ukraine, with 510,000ha of leased farmland. It focuses mainly on sunflower, it also has corn and wheat crops. It is the largest producer of non-GMO corn globally. The EBITDA for the farming sector was ~$302M LTM, an increase of 125% comparing FY20, and LTM. One of the reasons for the increase is the higher wheat and corn prices that helped Kernel boost its margins.

Source: Investor Presentation

Source: Investor Presentation

Ukraine land reform

Similar to what is currently happening in India, Ukraine has been trying to change the obsolete laws surrounding farmland ownership. These laws have hindered the agricultural sector growth in the region, and the changes could be beneficial for the country and Kernel in particular.

Up until this point, Ukraine had a moratorium on land sales, so individuals and entities could not sell their properties. The law was meant to protect landowners from being taken advantage of by large corporations or oligarchs. For years this has limited foreign investment in the country, and the World Bank estimates that Ukraine’s GDP could grow as much as 1.5% if the ban was lifted.

President Zelenskyy has slowly started to lift the ban. Starting this month, Ukrainian citizens will be able to purchase farmland up to 100ha. In 2024, the ban will be lifted for legal Ukrainian entities, which will be able to purchase up to 10,000 ha of land. This could be a major tailwind for Kernel, and it might be able to reduce fixed costs finance land purchases, and ultimately increase its margins slightly. Given that 10,000 represents ~2% of all the farmland Kernel uses, this new legislation opens the door for further reforms. Many have pointed out that the ban on farmland sales to foreigners is limiting the investment in agriculture in Ukraine. A referendum will be conducted so that Ukrainians can decide if foreigners should be granted the right to purchase farmland.

Kernel results

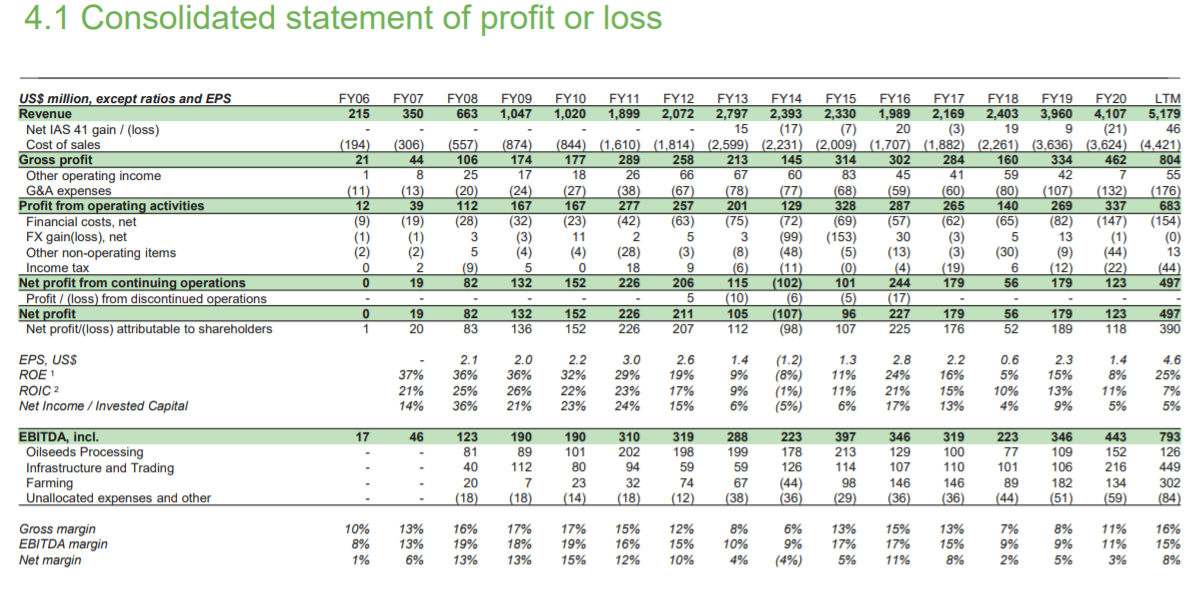

Kernel had a strong performance, boosted by higher sunflower oil prices. Revenues for the quarter increased 66% YoY to ~$1.729B, and it registered an EBITDA of ~$111M. Kernel’s strong performance has been constant over the years.

Source: Investor Presentation

Source: Investor Presentation

Higher prices of sunflower oil were the main contributor to the improvement in results and margin expansion. Despite the lower crop yields due to a drought, the results remained very positive, and Kernel continues to grow. Kernel continues to create shareholder value, with continuously growing revenues, earnings, cash flow, and equity value.

Source: Investor Presentation

Source: Investor Presentation

Valuation

Over the last twelve months, Kernel has achieved ~$5.179B in revenues, and an EBITDA of ~$793M. Margins have also increased, with EBITDA margin expanding to 15.3%, and net margin to ~7.5%.

Currently, the market cap is ~1.1B, which considering the sales and EBITDA seems deeply undervalued. Earnings per share LTM were ~$4.64, which gives the stock a price-to-earnings of ~3.25. Free cash flow over the previous twelve months was ~$394M, given the market cap it trades at ~2.8x free cash flow. If we take into account the lower CAPEX in FY22, it trades at under 2x estimated free cash flow in 2022, if the underlying commodity prices and supply and demand dynamics remain stable.

Capex

Management is estimating lower CAPEX for the next few years, given the completion of several projects over the last years. Since 2018, the total CAPEX was ~$883M. It included an additional 200k ha of leased land, construction, and improvement of storage facilities, construction of a new export terminal, and further investment in railcards. Until 2022, Kernel will complete the construction of an oilseed processing plant, with the co-generation of heat and power units. The whole project required ~$349M to complete and it is expected to boost EBITDA over the coming years. The estimated CAPEX for 2021 is still high at ~$179M, but the projected CAPEX for FY22 is just ~$8M. This means that if wheat, corn and sunflower oil prices remain at this level, free cash flow in FY22 should reach ~$570M.

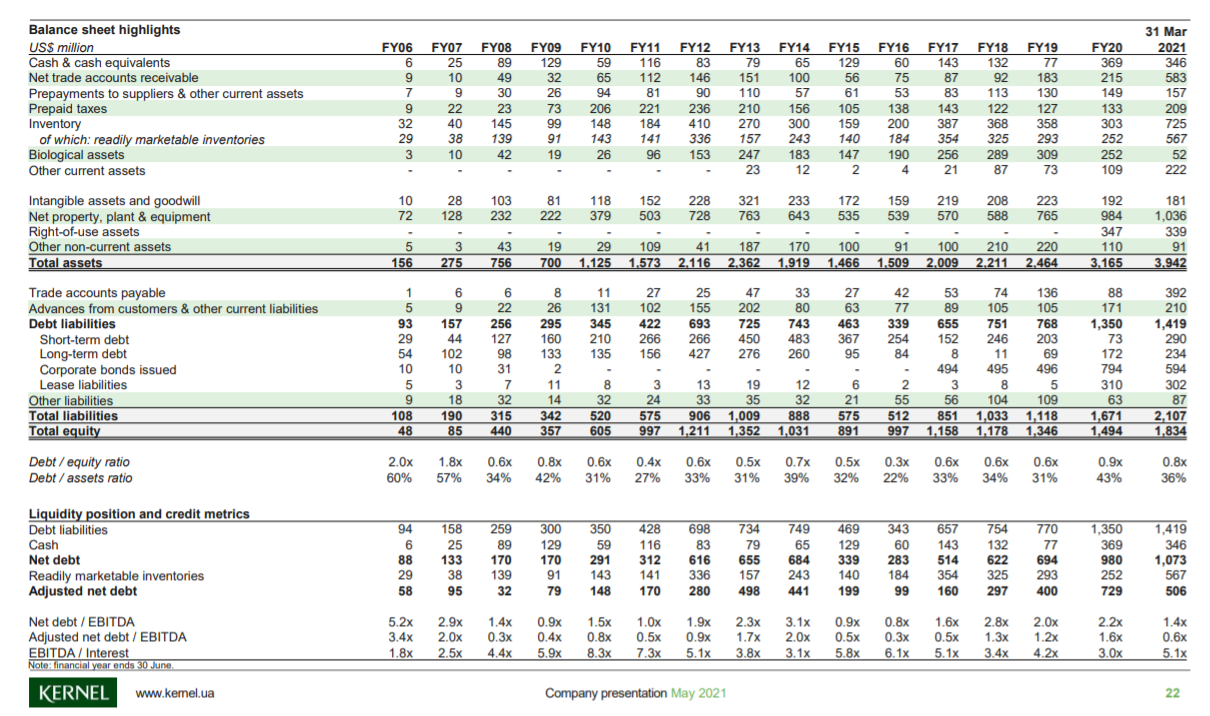

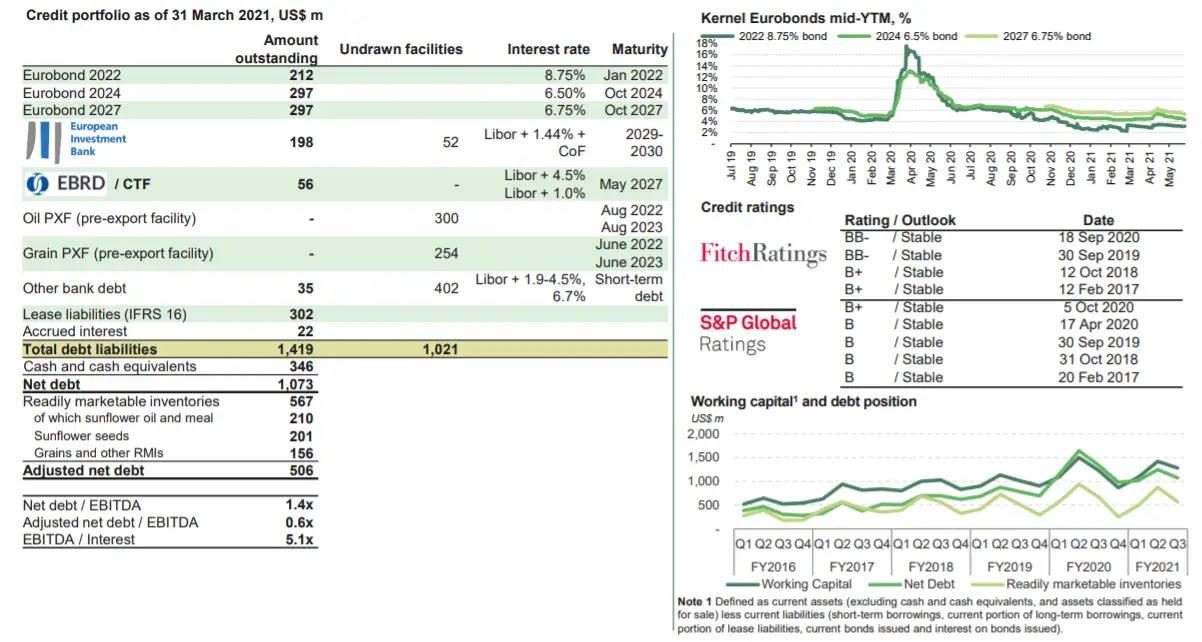

Debt

Kernel does not have the ability to finance its debt at very low rates, given its risk profile. Even considering that fact, the credit ratings point to a stable outlook. With Fitch assigning a BB-, and S&P assigning a B+.

Source: Investor Presentation

Source: Investor Presentation

With total debt and liabilities at ~$1.419B, and net debt remains at ~$1.073B - net debt is just 1.4x EBITDA. Although the interest on its debt is relatively high when compared with other similar companies in the EU and US, we believe the reduced CAPEX by FY22, will allow Kernel to refinance and repay some of its debt if needed. Credit ratings might improve given the additional ~$171M in cash flow the company will have. It can also choose to pay down some of the high-interest debt and clean the balance sheet. Although we would like to see the EBITDA/Interest ratio as low as possible it is at 5.1x. Representing the increased investments Kernel has made over the last four years.

Catalysts

Sunflower oil exports reduced

With exports in both Russia and Ukraine expected to be lower in 2021 and 2022, we could see a shock in supply globally. This could certainly boost sunflower prices, as many regions in the world depend on exports from Ukraine and Russia. Higher margins in the sunflower oil segment are expected throughout 2021 and into 2022.

Land reform

Although legally Kernel will only be able to acquire ~2% of the land it currently uses - the Ukrainian land reform could open the door for further legislation.

Founder and Chairman of the board owns a majority stake

This is always a positive sign in most stocks that we analyze. We have seen in the past that founders tend to have their interests aligned with shareholders. Over the past fifteen years, Kernel has been well managed and has constantly created shareholder value.

Reduced CAPEX by FY22

Capex in 2022 is expected to be ~$171M lower than in 2021, and this should allow Kernel to produce significantly higher free cash flow. Another advantage would be the refinancing of its debt, or management could shift and start paying down debt aggressively. We could also see further investments over the long term.

Kernel risks

There are good reasons why Kernel is being valued so low, and the main one has to do with the local risks. Ukraine is certainly not the most desirable jurisdiction for most investors. That alone will not deter us from investing in the stock. In our view, the major risk is the presence along the Ukrainian border of the Russian military. A conflict between the two nations could have deadly human consequences, and it would certainly halt Kernel’s operations to a certain extent. In light of this, our exposure to Kernel will be somewhat limited, taking into account the possible risks.

Russia Ukraine conflict

The tension between Russia and Ukraine has been increasing in 2021. Russia deployed part of its army to its eastern border with Ukraine. This has led Western countries to condemn Putin’s actions and intent of destabilizing the region. Although Russia later committed to pulling its troops from the region, there are still ~100,000 troops stationed in the region.

Although Ukraine is an ally of NATO, it is not considered a member. For that reason, the involvement of the organization in the region will be limited. Ukraine has no way to stop a Russian invasion, without foreign help. Ukraine cannot withstand a full-fledged conflict with Russia. Ukrainian’s only hope is a western intervention to put a stop to Putin’s intentions.

If we take a look at the army budget of each country, we can start to see the huge gap in the quality of military equipment. Despite increasing its military spending by ~83.7% since 2016, Ukraine’s defense budget is still less than 10% of Russia’s. Last year it spent about $5.4B, the highest in Ukrainian history. Russia, on the other hand, spent $61.7B. If we look at the number of troops each country has, Ukraine has roughly 255,000 active militaries, a far cry from the almost 1.9M active Russian troops.

Conclusion

Kernel is one of those stocks that are too cheap to ignore. The overall quality of the company’s operations and management are displayed in the stellar results it has achieved over the last fifteen years. Nowhere else in the world are investors able to find a global leader, with the largest market share globally in such a segmented industry as agriculture at this kind of valuation. Given the risks associated with it, we will start with a smaller position, and monitor geopolitical developments in the region that could give us another buying signal - if things improve. Even considering the risks the stock has the potential to deliver triple-digit returns.

We are long KER. Read our disclosure.

Featured image source: Kernel