- $13M market cap with $11.28M in cash and equivalents

- Insiders own 38.14% of outstanding shares.

- $12M in base ARR, with $12 million in contract value, and 94% customer retention.

- Investing $4M over the next 3 quarters to expand sales force and grow internationally.

Data Storage Corporation (NasdaqCM: DTST) is a nanocap stock in a growing industry that trades in deep value territory, with plenty of cash in its balance sheet. It offers disaster recovery, cloud, and cyber security services.

It works by establishing long contracts with its customers for a monthly fee, it has a subscription-based business model with 7 data centers across New York, Massachusetts, Texas, Florida, North Carolina, and Canada.

It has over 400 customers, ranging from large companies to sports teams. The average contract is 36 months, and the most common monthly subscription price is $3,000/month.

With a market cap of $13M, the company has $11.28M in cash and equivalents or ~86.8% of its market cap. Plus, it has $2M in accounts receivable, with just $3.57M in total liabilities. Additionally, its contracts generate $12M in ARR, and with a 94% customer retention rate, revenues are very stable.

The only analyst covering the stock estimates $1.7M in free cash flow for 2023 if revenues are the same as in 2022. However, the company is investing $2M to grow its sales force and another $2M to acquire customers overseas. Discounting the cash it has at hand and considering the $4M it will deploy until the first quarter of 2023, the company is trading at ~3.4x 2023 free cash flow estimates, which is deeply undervalued. This is not even accounting for the $2M in accounts receivable.

Data Storage Overview

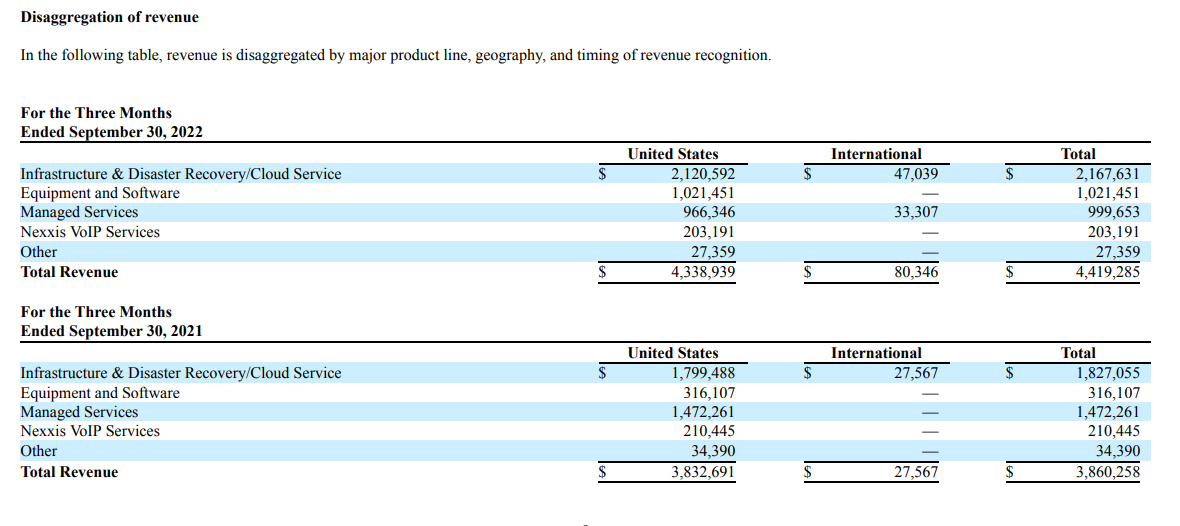

Cloud is still a significant part of Data Storage’s operations, and it is an important segment. In 2021 the cloud segment revenues were $8.2M or ~55% of the $14.9M total revenues. With the recent acquisition of Flagship, the company is slowly diversifying its revenue segments. While the cloud is still an essential revenue component, it represented under 49% of 3Q22 total revenues.

Source: 10-Q

Since last year the company has also grown its international revenues by over 191%, which shows the importance of investing more capital in acquiring customers overseas. Another important observation is that since 3Q21, all of the segments' revenues have grown, showing that the company still has a long growth runway.

Investing in its sales force and international growth

Until the end of 1Q23, the company will deploy $2M to grow internationally and $2M to increase its sales force.

Considering that the most common customer contract is $3,000 a month and the average contract duration is 36 months, it equals $108k in revenue. Therefore the $4M investment to increase its sales force and grow internationally only needs to acquire 39 new customers to generate $4M in revenue. This is not even considering the 94% customer retention rate in its cloud business, so Data Storage should be able to retain new international customers.

In the last earnings call, the management also reiterated how they are witnessing an increase in monthly payments by each customer and how contracts are being extended, sometimes up to 60 months.

Flagship Acquisition

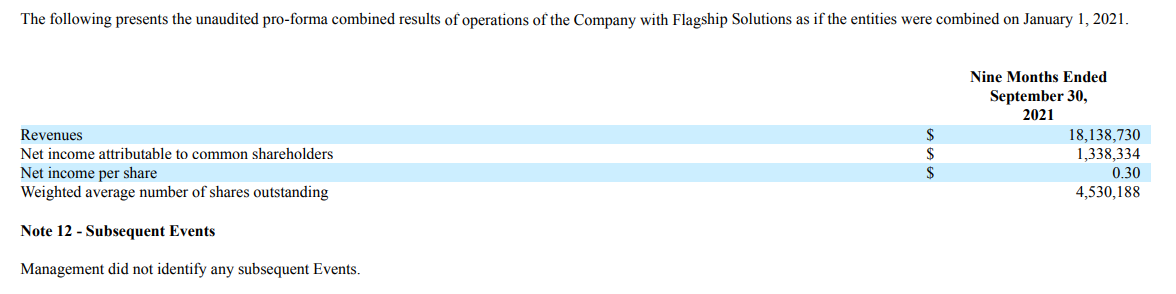

Data Storage acquired Flagship for $5.5M at a multiple of 8.4x EBITDA. The acquisition allowed the company to diversify its services while adding some large clients and the ability to cross-sell. Flagship also had 212k in cash and ~$1.39M in accounts receivable, with just $1.29M in liabilities.

Its performance over the last 9 months has also been exceptionally good, generating over ~$1.33M in net income, and given the purchased price, the company is trading at slightly over 3x earnings, which shows how good of a deal it really was.

Source: 10-Q

Estimates for 2023 and Valuation

Only one analyst is covering the stock, and its estimates for 2023 are very optimistic, with EBITDA expected to be $1.8M and FCF of $1.7M. Revenues are expected to be in line with 2021, at $23.3M.

There are very few companies valued as low as Data Storage, especially when we consider the amount of recurring revenues the company has, plus the value of the contracts with its customers.

Even if revenues stay flat in 2023, the company has 86.8% of its market cap in cash and equivalents, plus ~15.4% in accounts receivable, and it will generate 13% in FCF in 2023. Additionally, the $4M investment could push revenues and profits even higher.

The flagship acquisition has proven that the company knows how to acquire and integrate other businesses, and take advantage of the synergies created.

Discounting the cash and cash equivalents, the company is basically trading under 1x 2023 FCF, which shows how the stock is deeply undervalued.

Risks

Illiquid

Data Storage is a highly illiquid nanocap, and with insiders owning over 38% of the shares outstanding and institutions owning 9.22%, the float is just 4.19M shares. Moreover, the stock has a very low trading volume, in fact, in some weeks, the total number of shares traded is just 35k.

Be aware if you are planning on building a significant position in the stock, that it might be difficult to acquire shares and also sell them.

Dilution

Outstanding warrants can bring an additional $13M, with a strike price of $6.5, which could also dilute existing shareholders, and while there is a slight risk of dilution, the Flagship acquisition shows that the management knows how to allocate capital properly, and therefore the dilution shouldn’t through the exercised warrants shouldn’t worry existing shareholders.

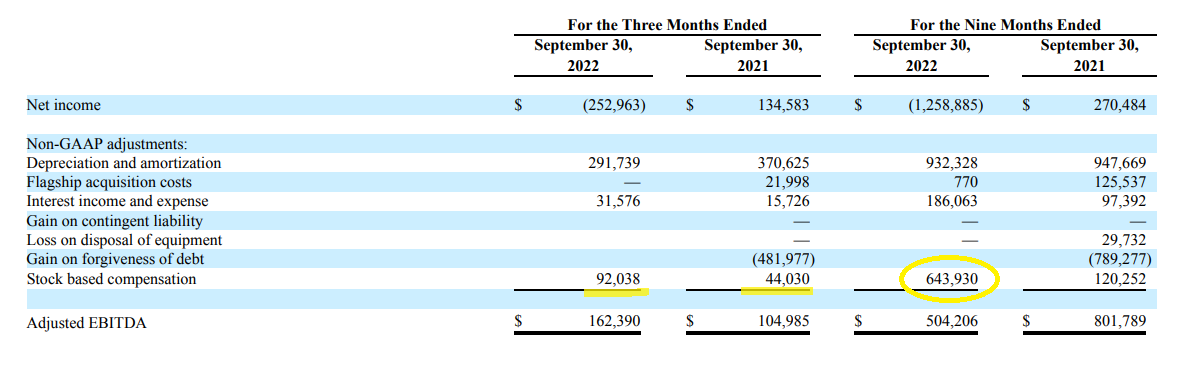

Stock-based compensation has also increased, especially over the last 9 months. This presents another risk for further dilution of existing shareholders.

Stock-based compensation

While stock-based compensation is something common in every company, the situation is different when it comes to Data Storage. Over the last 9 months, stock-based compensation was higher than the adjusted EBITDA, leaving current shareholders and investors wondering if it makes any sense to invest in the business.

Source: 10-Q

On one hand, it is difficult to attract and retain high-level talent in a small company and still offer competitive pay, but at the same time, the current level of stock-based compensation is hurting the company’s bottom line and shareholders.

Conclusion

Data Storage is undoubtedly a risky stock, but the valuation is as good as it gets. We need to consider how large the total addressable market for its services is and how it can easily and quickly grow revenues by 2 or 3 times in just 5 years. The valuation is extremely attractive, and trading at 1x 2023 FCF ex-cash the stock is as cheap as it gets.

The management also seems extremely proactive and capable of delivering more growth. The company’s balance sheet is clean, with plenty of cash to deploy. Additionally, with the contracts in place and a very high customer retention rate, Data Storage’s revenues and profits can be easily estimated, which gives the company a stable cash flow generation.

We also shouldn’t rule out another acquisition similar to Flagship and expand its customer base with the ability to cross-sell and retain even more customers.

We have no position in any of the stocks mentioned in the article.

Read our disclosure.