- Declining sales and earnings will continue to pressure the stock price over the coming quarters.

- Over 17% of its market cap is in cash and cash equivalents with very little debt.

- Over 11% free cash flow yield considering the current valuation.

- An 8.4% dividend yield and nearly 20% insider ownership.

- Attractive valuation for long-term investors with growth ahead.

Micro-Star International (TW:2377), or MSI, is a prominent gaming hardware manufacturer with a global presence that has benefited from the pandemic and seen a surge in sales and profits. However, over the last 4 quarters, the company’s revenues and earnings declined, and so did its stock price from ~$T184.5 to T$125. Despite the declining revenues, MSI’s 2023 EPS is still expected to be over T$12, which gives the stock a P/E ratio of just 10. Additionally, the company has barely any debt at just under T$700M, and it has a strong cash position of over $T18B.

Gaming market

MSI offers a full range of products for gamers, from desktop computers to hardware, laptops, and peripherals. Although MSI's presence in the gaming hardware market is small, it is a significant player in underdeveloped countries, where its pricing makes a significant difference for gamers.

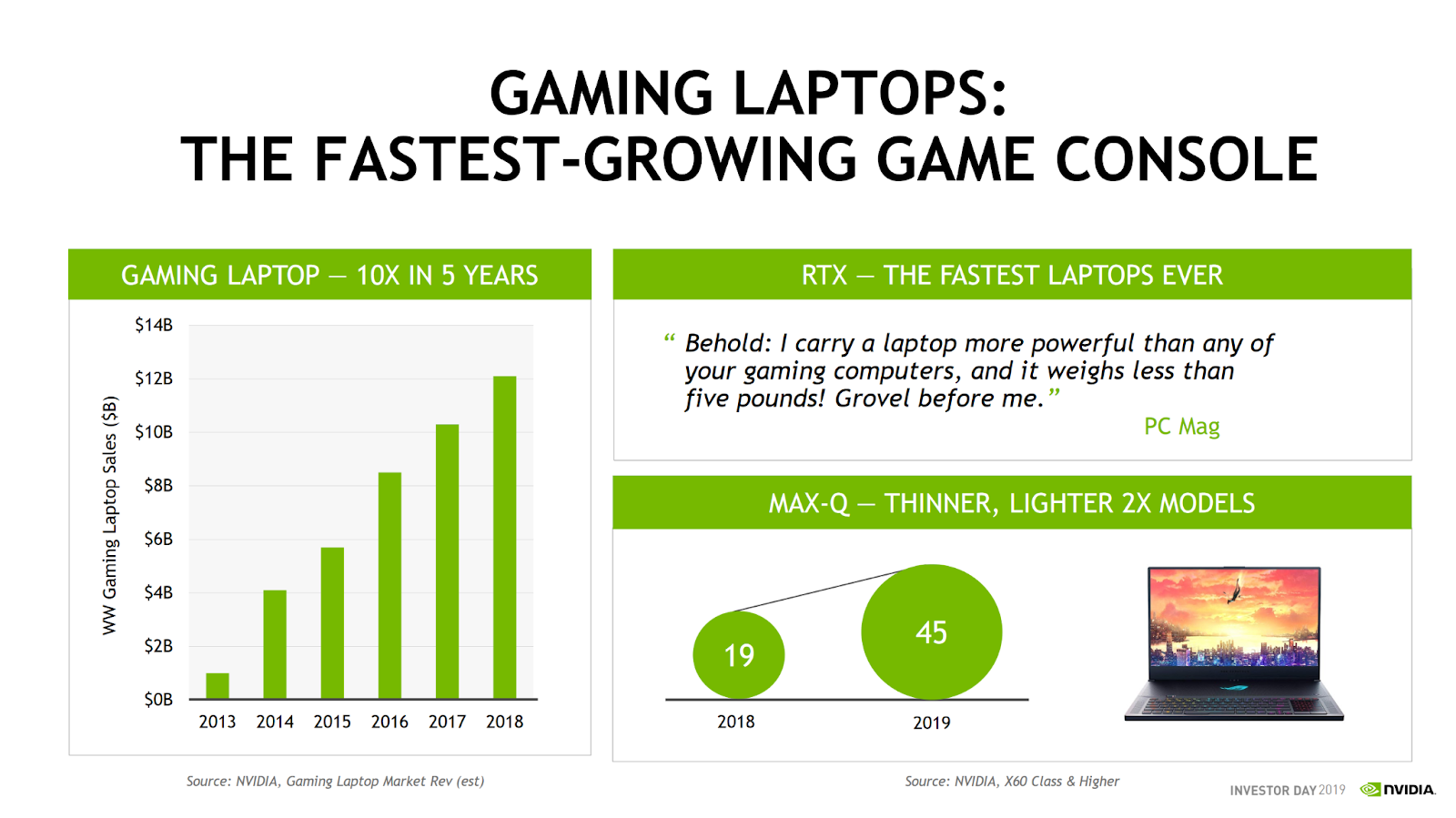

The PC hardware gaming market is one of the fastest-growing gaming segments, while it was valued at $35.9B in 2021, it is expected to reach $145.93B in 2030. MSI has been able to establish itself as one of the best value-for-money brands in the gaming space, especially in the laptop segment, where it has been able to remain highly competitive

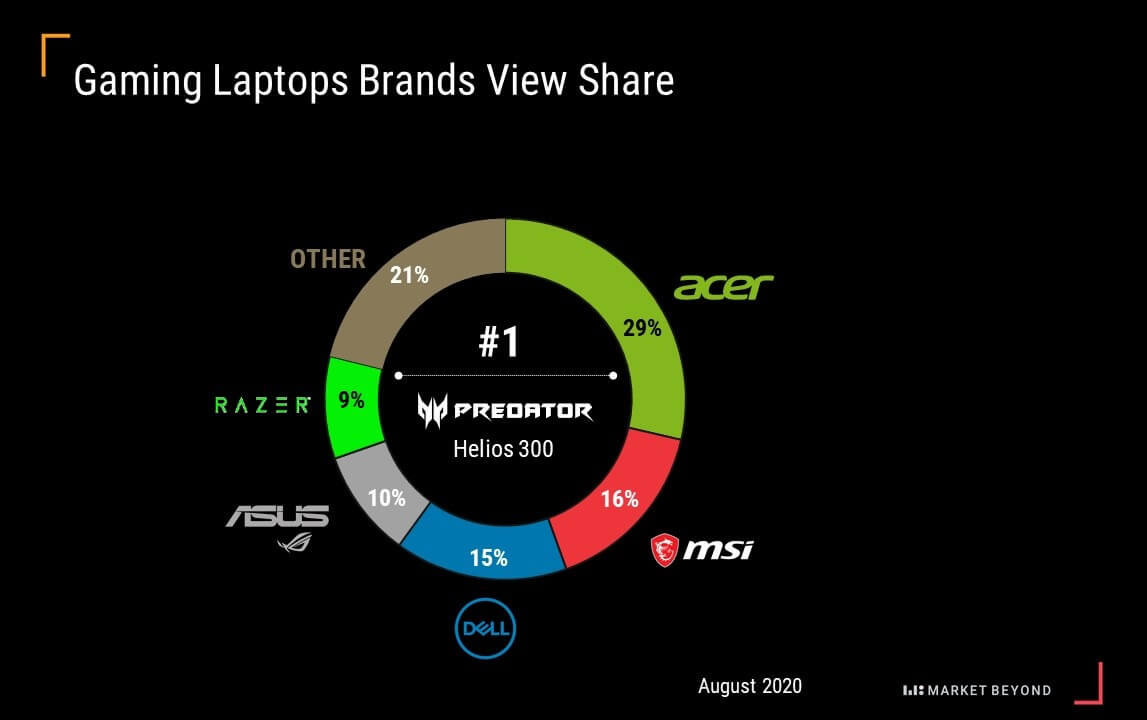

Market share

MSI has maintained a significant market share of the gaming laptop market, and it has even remained more competitive than other large companies in the space, including Dell, Acer, Asus, and Razer. One of the main reasons has been its low price, which makes MSIs products very attractive for the low-end gaming consumer.

Source: The Market Beyond

Additionally, gaming laptops are the fastest-growing segment in the PC gaming space. The laptop’s portability makes it a strong selling point.

Soon after the pandemic started, PC and PC hardware sales increased, and in fact, PCs and laptops were by far the biggest beneficiary of the work-from-home movement that the pandemic ignited.

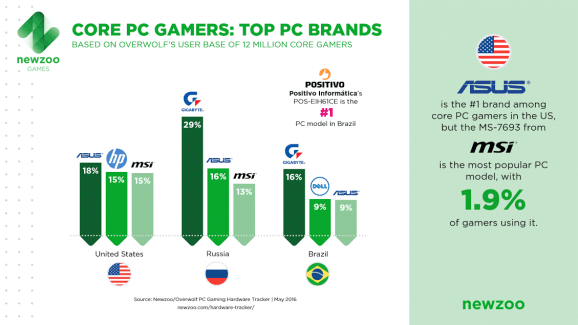

However, with the pandemic ending and many employees returning to the office, PC and PC hardware sales have declined. Despite not being the market leader, MSI computers are some of the most popular choices among gamers.

Source: NewZoo

Pandemic boosted results

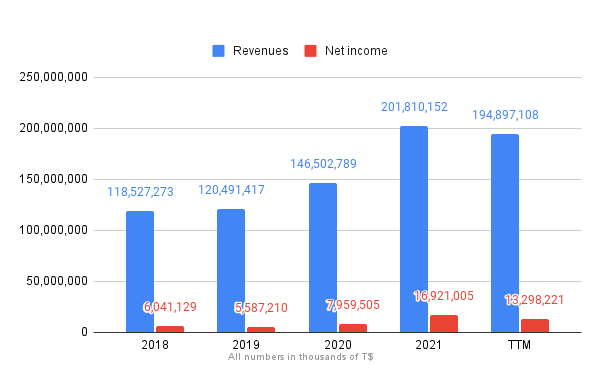

MSI benefited from the pandemic and the increased demand for gaming laptops, computers, and peripherals. The company’s revenues in 2021 increased by ~37.8% compared with 2020, and profits increased by 112%.

Source: Author

Since then, over the last 4 quarters, revenues and profits have continuously declined. In 3Q22, revenues were just T$38.57B and earnings of T$1.61B. Despite that, the profits over the last 9-month profits stand at T$9.4B or roughly ~$300M, which is still significant compared to the current market cap of $3.41B.

MSI Stock Price

The stock price has declined since the high in 2021 following the stellar results, but it currently sits at around T$125. We could see the stock price decline even more over the coming quarters if the company’s results are lower than analyst estimates.

Source: TradingView

MSI valuation

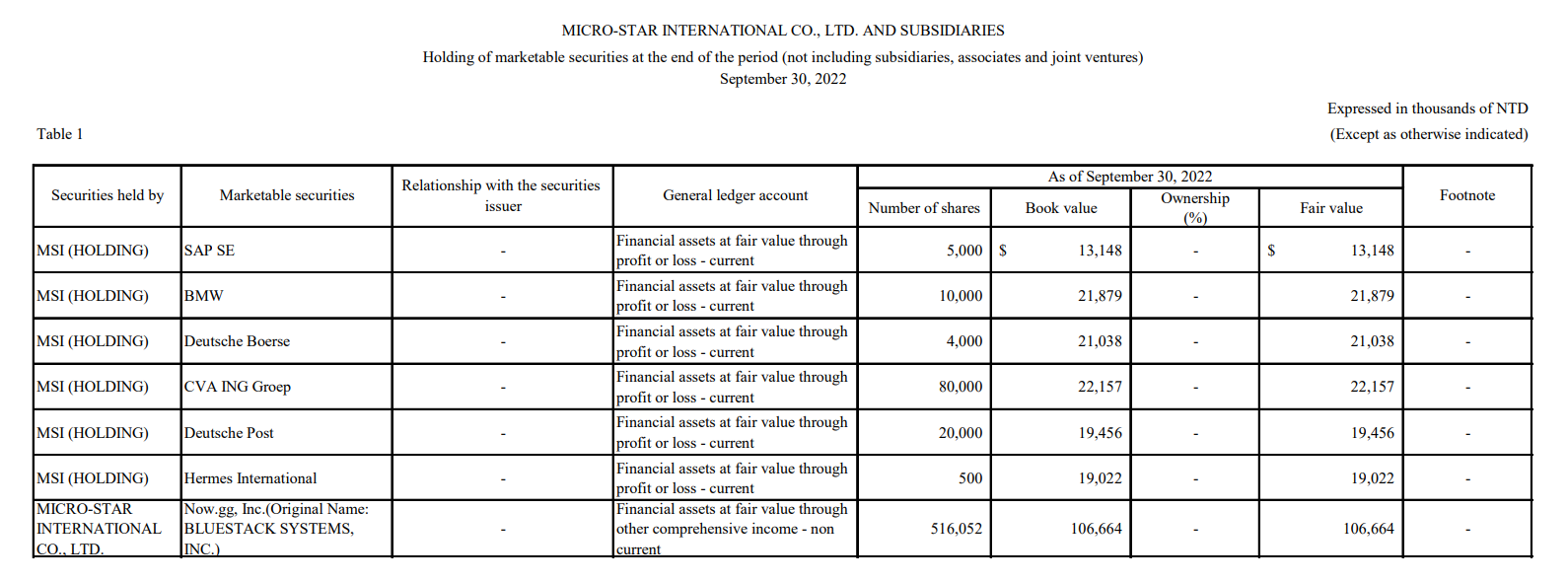

MSI currently has a market cap of T$105.6B, with T$18B in cash and equivalents and $T18.57B in accounts receivable. The company also has a small portfolio of securities valued at ~T$223.4M, which includes some well-known stocks.

Source: 3Q22 Results

$T30.66B in inventories that the build-up following the chip shortage and the increased demand for its products. The declining revenues and the high level of inventories could be a reason for alarm, but we will see how the company can manage it going forward over the coming quarters.

In 2021 the company generated over T$11B in free cash flow, and the TTM free cash flow is currently T$12.24B, so it is far to assume that MSI will be able to maintain FCF of over T$10B.

Assuming the company can maintain its free cash flow at around $T10B a year, ex-cash, it is trading at 8.76x free cash flow, which gives it a free cash flow yield of 11.4%.

Considering its strong position in the gaming market and its products are some of the best in the low-end gaming segments, it is an attractive valuation.

Insider ownership of 19.58% is also a positive sign and should give investors more confidence in the stock. With just T$654M in debt and generating over T$10B in free cash flow every year, there is no risk of bankruptcy or any short-term headwinds that could put the company at risk.

Declining revenues and profits are expected over the coming quarters until demand for gaming laptops, PCs, hardware, and peripherals stabilizes.

MSI is currently trading at an attractive valuation, considering it holds a lot of cash, it has close to no debt, and it is still generating a lot of free cash flow, with a long growth runway ahead. Despite the expected decline in revenues for the last quarter of 2022 and the lower earnings in 2023, the stock still seems attractive.

We should see revenues and earnings stabilize in 2023, and at this point, monitoring the stock and adding it to your watchlist should be the best approach. Adding a small position is also an option, but it seems that the lower expected results in 4Q22 and the uncertainty surrounding the sales and earnings in 2023 could put additional pressure on the stock price.

Nonetheless, if the results are worse than expected, MSI could trade under T$100, and at those levels, the stock seems like a solid long-term investment, with growth ahead and plenty of upside.

MSI dividend

MSI currently has an 8.5% dividend yield, but given the decline in sales and earnings, at some point, we can expect a lower dividend in the future. At the current valuation, that implies around T$8.87B in dividends paid to shareholders and considering the current earnings over the last 9 months of T$9.4B, the dividend might be lower over the coming years.

Possible acquisition

Given the current valuation, MSI also seems like an attractive acquisition target, either for vertical or horizontal integration. The company’s market cap of $3.41B makes it an enticing acquisition while generating over $300 million in earnings yearly, making it a possible target for acquisition or even a merger with other companies in the space.

Risks

Taiwan tensions

Taiwan and China tensions are one of the principal risks of investing in MSI. The results of the recent Taiwan local elections have pushed Taiwanese president Tsai Ing-Wen to resign following the bad results.

The opposition party with strong ties to China seems to be taking the political leaders in the country. While it is too soon to say how this can influence the businesses and economic activity in Taiwan, it seems like it could be a way to de-escalate the tensions in the region.

We could even see Taiwanese stocks decline across the board following the election results and the president's resignation.

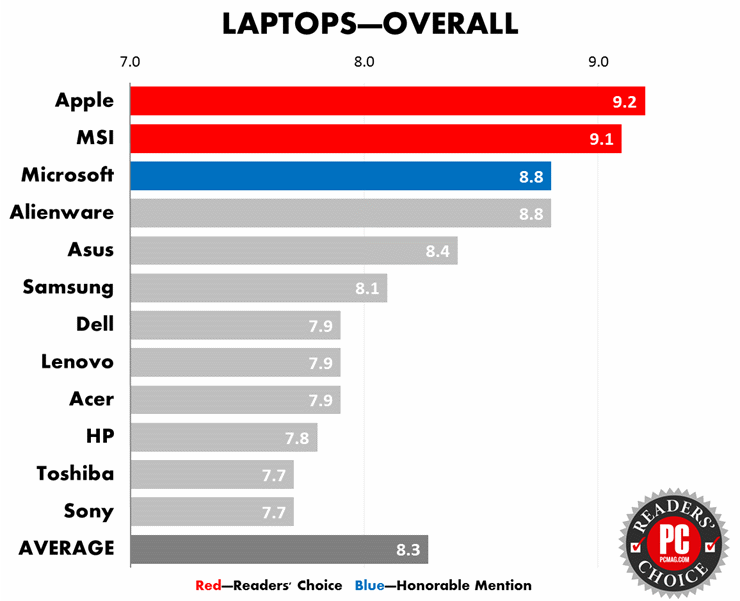

Bad reviews

MSI has had a bad reputation among some gamers, and bad reviews, with many customers complaining about late deliveries and faulty products. Compared with other gaming brands, it seems that MSI has a bad reputation in terms of customer service and after-sales support.

However, gamers still choose MSI products because they offer more value. In some of the surveys conducted consumers seem to favor MSI’s products.

Source: PC MAG

This remains a risk for the company and its shareholders, as the lousy reputation could hurt future sales and push MSI’s market share lower.

Conclusion

MSI is experiencing declining revenues and profits after the pandemic boosted its sales, and it seems like the stock will soon find its bottom.

Despite the lower revenues and earnings, MSI is still trading at an attractive valuation, even considering the lower free cash flow over the coming 2 to 3 years. Analysts are still estimating earnings per share slightly over T$12, which puts the stock at a price-to-earnings of just 10.

Given the expected declining revenues over the next quarter, you should wait until the stock price stabilizes, but over the next few months, it could be a chance to add MSI to your portfolio at a great price.