Unknown to many, CK Hutchison (HKSE: 0001) is one of the biggest Chinese conglomerates operating in multiple segments. We believe CK Hutchison is undervalued when considering its ability to generate future earnings and the value of its assets.

The company’s holdings span a wide variety of industries. From retail to energy, ports, infrastructure, telecommunications, the list goes on. They are also well distributed across the world, with operations in over 27 countries.

CK Hutchison is trading at an attractive valuation, given that the sum of its parts has a higher value than the price indicates.

CK Hutchison Segments

Most of CK’s revenues come from its retail segment. Which represented 39% of revenue in the first half of 2020. Given that retail has lower margins, 34% of the total EBITDA is actually attributed to its telecommunication business. Which obviously has the highest margins.

Source: 2020 Interim Report

This is attributed to the unprecedented oil price action we witnessed in early 2020. When oil was even trading at a negative price. CK Hutchison ended up booking a loss on Husky Energy. Husky Energy has recently changed its name to Cenovus (NYSE: CVE). Management has decided to cut its stake from 40.2% to 15.7%. CVE contributed negative HK$2.751B to CK’s EBITDA.

The segments that contributed the most to EBITDA are telecommunications, infrastructure, finance, and investments, with 34%, 29%, and 21% respectively.

CK Hutchison's Cellnex Deal

In 2020 CK Hutchison reached an agreement with Cellnex Telecom (BME: CLNX), to sell part of its telecommunications portfolio in Europe. The deal valued at €10 billion or nearly $11.8B, included an initial payment of €8.6B. The remaining amount will be paid with new shares. CK Hutchison received a 5% stake in Cellnex. Cellnex currently has a market cap of ~€22.25B, the 5% stake translates into ~€1.113B.

CK’s telecommunication segment is by far the most profitable and interesting. In a way, it is a shame to see the company divest part of its core holdings. Nonetheless, the price paid was more than fair, and CK still retains 5% of CLNX.

Impact on Earnings

As of June 2020, the 3 Group Europe, CK’s subsidiary that holds its European telecommunication assets reported HK$40.524B in revenues and HK$14.449B in EBITDA. Using the reported earnings and revenues for the first half of 2020. We can expect CK’s revenue to drop ~21% and EBITDA to decrease by 30%.

Given that CK’s market cap was ~HK$206.5B when the deal with CLNX was announced. The company essentially sold its 3 Europe Group for ~45% of its market cap. Given the expected decrease in revenues and EBITDA, and the stake in CLNX it seems CK got the better end of this deal.

Bear in mind that 3 Group Europe's customer base has been declining. Registered customers dropped by 6% from June 2019 to June 2020. The number of active users, the ones that generate revenue by outgoing call, incoming call, or data use has also declined by 7% from June 2019 to June 2020.

Valuing CK Hutchison

The total market cap of the company is ~$31.5B. Given the recent deal with Cellnex, CK Hutchison is currently in a great position. The company reported HK$140.147B of cash and equivalents in the first half of 2020 or roughly $18.08B. Add the $10.44B of initial payment from the Cellnex deal.

The company will have at least $28.52B. Given CK Hutchison’s cash position and market cap, the stock is trading under cash. This sort of opportunity doesn't come around every day. The cash position relative to the market cap is only one of the ways we can conclude that CK Hutchison is undervalued.

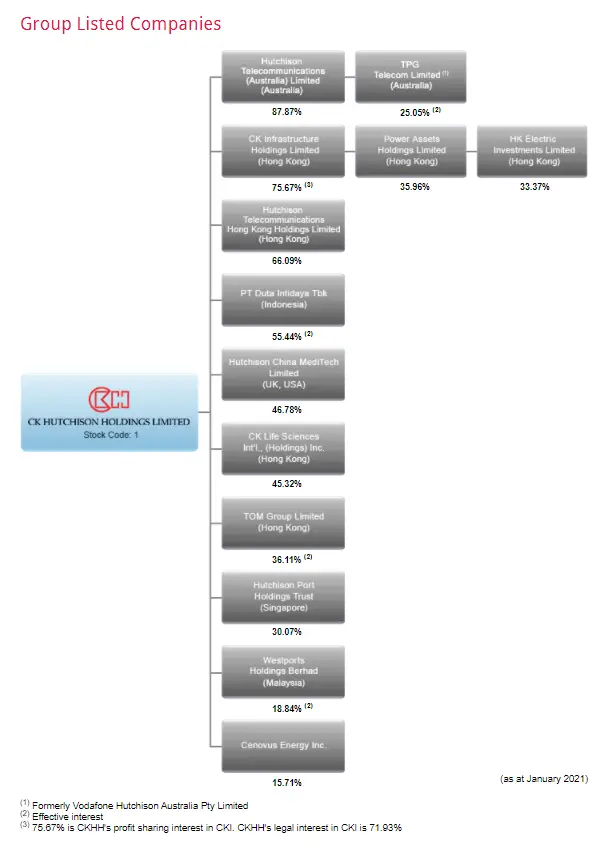

Holdings

Source: CK Hutchison

Source: CK Hutchison

If we analyze all of CK’s holdings of other companies we can also reach the conclusion that the stock is trading under its fair value.

Through its subsidiary, CK holds 25.05% of TPG Telecom (ASX: TPG). TPG has a market cap of ~AU$12.77B. CK’s stake is worth ~HK$18.87B.

It owns 66.09% of Hutchison Telecommunications HK (HKSE:0215), which has a market cap of HK$7.08B. CK’s stake is worth ~HK$4.68B.

After it cut its stake it now owns 15.71% of CVE, which has a market cap of ~$15.65B. It is worth ~HK$19.42B.

Its 5% CLNX stake is now worth ~HK$10.03B after the deal was concluded.

CK Life Sciences (HKSE:0775) was spun off from CK Hutchison, and the company owns 45.32%. Its stake is worth ~HK$3.6B.

CK Infrastructure (HKSE:1038), which was also spun off has a market cap of ~HK$121.27B. CK’s stake is 75.67%, valued at HK$91.77B. In turn, 1038 owns stakes in both Power Assets (HKSE:0006), and HK Electric Investments (HKSE:2638). CK through its ownership of CK Infrastructure owns 35.96%, and 33.37% of 0006 and 2638 respectively. Given the stakes in both companies and its current market valuations, it translates into roughly HK$58.36B

Hutchison China MediTech (NASDAQGS: HCM) is another company in which CK has a stake. Its market cap is ~$3.95B. With a stake of 46.78%, CK’s stake is valued at ~HK$14.36B.

CK also owns 30.07% of Hutchison Port Holdings (SGX: NS8U), CK’s stake is worth approximately HK$4.8B.

Other investments

CK also owns some investments that I have not mentioned. AlipayHK was a joint venture between Alibaba (NYSE: BABA) and CK. Each of the companies owned 50% of the said joint venture. Given the recent polemic situation preceding Ant Financial IPO, CK decided to cut its stake in Alipay HK. CK cut its stake to 39.7%, it is at this moment fairly difficult to value both the joint venture and CK’s ownership. Since the company is private, we will have to wait for the annual report of 2020 to actually understand at what valuation CK divested 10.3% of Alipay HK.

Not only is the cash position higher than the market cap. The company owns multiple assets that given the market cap it makes the stock seems way undervalued. If we add up all the value of CK’s stakes in the companies mentioned, we arrive at a rough value of over HK$200B. In fact very close to the current market cap of ~HK$234.45B.

Final Thoughts

CK Hutchison presents a rare value opportunity. It is both a value stock and an asset play, that has plenty of upside from here. The company is well diversified in its operations, and revenue is distributed across multiple continents. At these levels there is very little downside in the medium term, presenting a solid margin of safety.

CK Hutchison has consistently rewarded shareholders with dividends over the past. Although

the deal with Cellnex will impact revenues and earnings, the amount received allows CK to improve its balance sheet. Turning its attention to other investments. The fact that the company’s operations are well diversified and well-distributed geographically is a big advantage. It protects investors from any downturn in a specific industry or geographically.

The market is clearly not valuing CK properly, based on its earnings and its holdings in multiple companies. The stock under HK$65 seems like a complete bargain price.

We are long 0001. Read our disclosure.

Featured image source: Storyblocks