- Greatview Aseptic Packaging is trading at a 12% free cash flow yield.

- Dividend yield of 8.36% with a high payout ratio.

- Earnings will be lower during 1H21 due to higher raw materials.

- We think the stock trades at a discount relative to its long-term outlook and defensive nature of the sector.

Greatview Aseptic Packaging (HKSE: 0468), manufactures and distributes paper, and plastic packaging mainly for the food industry. Although it has not been one of the best-performing stocks in the past, we like its defensive nature. The company has manufacturing facilities in China and Germany and sells its products worldwide.

It has consistently increased revenues and profits, benefiting most of the shareholders. Due to the intrinsic nature of its business, Greatview is often an overlooked stock by most investors, who seek higher returns. We think Greatview deserves a second look as a very important player in the packaging market in China. Its business has a high barrier to enter, and for investors looking for safe positions, or with a lower risk tolerance it could be an interesting addition to your portfolio.

Greatview Aseptic Packaging Investment Thesis

We have followed Greatview for a while, and the stock has always been fairly underpriced. Lately, the company announced that due to increasing raw material costs, directly affected by inflation - its profit for the first half of 2021 will be lower than in 2020. Given the expected lower profit, the stock has started to trend lower, and we think it could reach a level around HK$3, which could be a buying opportunity.

Annual consumption of non-alcoholic beverages in China has continued to grow, even at a slower pace. It is expected that consumption will reach 104B liters this year alone. Greatview is well-positioned to reap the rewards of the increasing consumption of packaged drinks.

Results

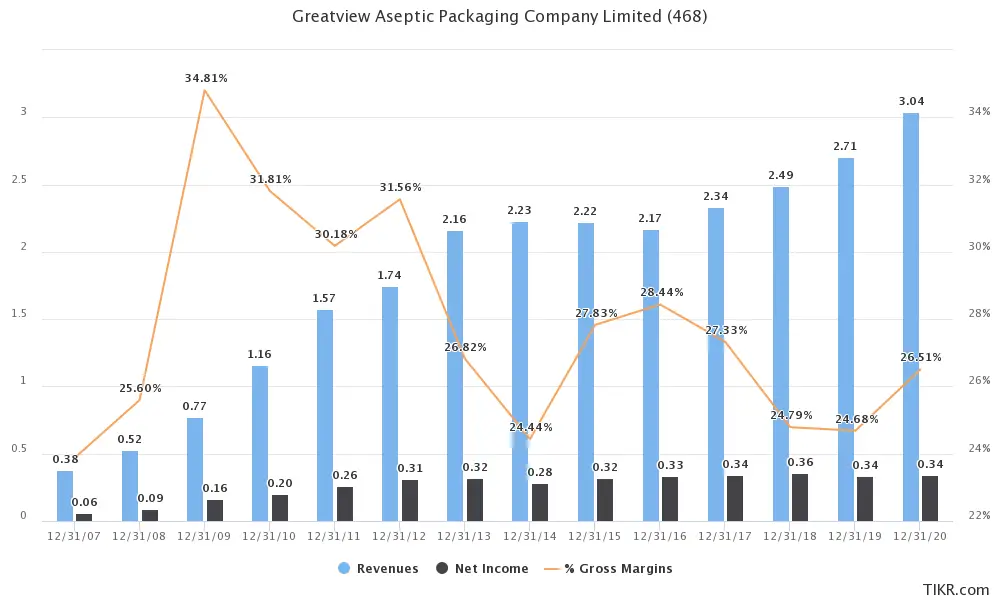

The pandemic had a meaningless impact on operations, and the company still managed to present good results. It increased revenues by 12.3%, and gross profits by 20.6%, compared with 2019. The EPS increased 4% YoY. Lately, with the increased inflation, Greatview has seen prices for raw materials increase.

The company needs to source these raw materials to produce the packages, and its margins are directly affected by the increase in costs. Although we think this is a momentary slump in gross margins, the company has pricing power. It should be able to pass along to its customers, the increased cost to source raw materials.

According to the announcement, the profit expected for the first half of 2021 is around RMB137M and RMB147M. This translates into a projected profit of HK$170M. Considering the market cap at the moment of this writing, it currently trades at a price-to-earnings of 13.76.

Considering the high valuations across all markets, this seems like a fair price to pay for such a strong and defensive company. Since it went public, Greatview has managed to constantly grow revenues consistently, and margins have remained somewhat stable.

(All numbers in billion RMB)

Source: TIKR

Greatview Aseptic Packaging Valuation

Greatview currently has a market cap of ~HK$4.344B, and the price-to-earnings based on the first half of the year results is a little under 14. When we look at the business cash flow, we see that Greatview generated RMB433.76M in free cash flow in 2020. This equates to roughly HK$521.6M. Based on that the stock currently has a free cash flow yield of 12%. This looks quite attractive considering the lack of undervalued securities in most markets.

On top of that Greatview has been paying handsome dividends to its shareholders over the years. Due to the nature of the business, CAPEX is low and it can return most of the profits to investors. Based on the dividend last year, which was HK$0.27, its dividend yield is currently 7.7%. This makes it a very interesting stock for dividend investors. The payout ratio is fairly high around 90%, but due to the low CAPEX, it does not affect the company’s ability to grow.

Conclusion

Greatview is well managed, and its business delivers consistent and predictable results. It has well-established long relationships with its customers and remains a good defensive stock. The growth going forward will most likely be in the single digits, but considering the price, it is a fair valuation.

We believe that once the company presents results, the stock price should continue to drop. Thus, around HK$3 a share, the shares look more attractive and give investors enough margin of safety. This is not a stock for every investor, as its growth prospects will be lower than some other industries. We think it has a place in some portfolios looking for more stable holdings.

Read our disclosure.

Featured image source: Twitter