The stock market is driven by earnings, in other words, growing revenues means nothing if you can't report earnings. Farfetch (NYSE: FTCH) has been unprofitable since its inception over 13 years ago, despite that the stock price has been performing extremely well. The company runs an online retail platform, and partners with over 1,000 different partners to offer their products to their one million active customers. By doing so Farfetch charges 30%-plus a commission on the sale. Given their business model the company has a limited stock and is protected against discontinued designs and products. The stock has soared over 600% since the March sell-off. Investors are too optimistic not only around the sector but around the company.

Overview

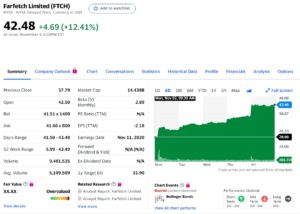

Shares were trading on the 2nd of November under $29, reaching a high on Friday the 6th of November of $43. The surge in price was driven by an agreement it reached with Richemont (SWX: CFR) and Alibaba (NYSE: BABA). Both companies agreed to invest a total sum of $1.1 billion in Farfetch, $550 million each. Artemis, an investment company founded by Kering’s (EPA: KER) CEO also boosted its stake in Farfetch by $50 million. The deal aims to conquer the Chinese luxury goods market, with the help of Farfetch's expertise in its online operation. The Chinese luxury market is expected to account for half of the global luxury sales by 2025.

Source: Yahoo Finance

According to the Financial Times:

“Under the agreement announced on Friday, Alibaba and Richemont put $300m each into Farfetch itself and another $250m each into a newly created unit called Farfetch China, which will include the marketplace’s operations in China. They will own 25 percent of the Chinese entity, and have an option to buy another 24 percent in roughly three years.”

The $300 million will be in the form of senior converting notes yielding 0%. Wells Fargo decided to upgrade the rating on the stock and put a price target of $42. The deal made Farfetch terminate the partnership it had with JD.com(NASDAQ: JD). JD had invested $397 million into Farfetch in 2017.

Acquisitions

Farfetch has made several acquisitions over the years, diversifying its operations. The acquisitions include retailers such as Browns, Toplife, and Stadium Goods for which it paid $250 million. To expand its marketing reach in the Chinese market it acquired CuriosityChina. The company has also acquired New Guards Group paying $675 million. The buying spree totaled over $1 billion, and despite that fact, the company has yet to show a profit. Condé Nast, which owns Vogue magazine, was one of the early investors in Farfetch. Worried about management decisions, Condé Nast decided last year to sell its nearly $300 million investment in the company. The decision was made over concerns that management was not allocating capital in the most efficient way with all the acquisitions.

Farfetch’s merger and acquisition strategy has not materially affected the company’s earnings. Not only that but with the acquisitions made in the retail space, the overhead costs increase and do not seem to be the best option. As an investor, we should be wary of companies who try to grow inorganically, as it may signal a selling signal, especially when they are not profitable.

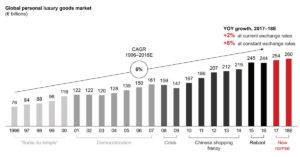

Luxury market overview

The luxury goods market has seen great growth in the last decade and should continue even if we experience a slight slump. Just like it happened in 2008 with the recession, luxury goods sales went down, and the impending crisis we might experience can negatively impact the market, as consumers refrain from spending money on luxury items.

Source: Brain

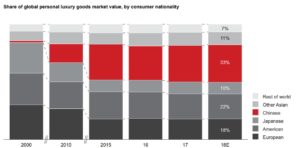

The luxury goods market has been growing exponentially in China. Farfetch's venture agreements with Richemont and Alibaba will try to reap the rewards. As the company combines its expertise in online sales with Richemont's products and Alibaba’s knowledge of the Chinese market.

Source: Brain

The Chinese consumers will become the most important in the space, and eventually European and American consumers should account for a little over 30% of the market by 2025.

Source: Brain

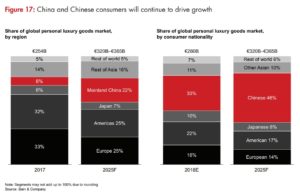

This is one of the reasons investors are so bullish on Farfetch, furthermore, the growth is expected to come from the online segment. Given Farfetch's position and operations, the company can capture some of the Chinese market share and establish itself as an important player in the Asian market. The online segment of luxury goods sales is expected to grow 150% by 2025.

Source: Brain

However, the pandemic has sent the global economy into a recession and sales should be affected. Given the number of unemployed people around Europe and the U.S., sales in the sector are expected to decline given the lack of spare money to spend on high-end clothes and accessories. China seems to be the only market to experience growth in the short term. The luxury goods market is cyclical and inevitably the cycle has come to an end. Therefore, investors should understand that despite the positive outlook in the long term the company might experience a tough period in the short term.

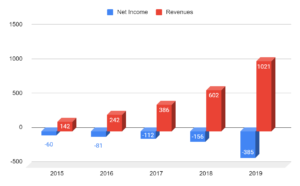

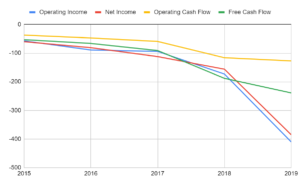

Fundamental Analysis

Since 2015 despite growing revenues nearly 10-fold the company has been struggling in operational terms, generating negative free cash flow, and the trend seems to continue.

(All numbers in thousands of $)

Source: Morningstar

(All numbers in thousands of $)

Source: Morningstar

The second-quarter earnings report shows that the company has managed to grow its revenues by over 90% YoY, but it also shows warning signs for the astute investor. But the dilution continues, and that is one of the reasons the loss per diluted share was not as bad comparing YoY. On another hand, Farfetch's finance costs are increasing at a great pace and that can be an alarming sign. therefore, the retail acquisitions it has made in the past were greatly affected by the pandemic. These seem to be some of the reasons the company sought out to make an agreement with Richemont and Alibaba.

Source: Farfetch

Source: Farfetch

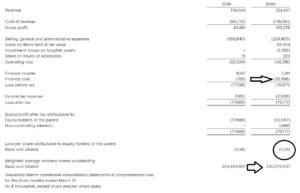

The latest earnings report concerning the third quarter shows that despite the revenue growth of over 71% YoY the company is still struggling operationally. Thus, the total loss after tax for the period was $537 million, and adjusted EBITDA was $(10) million. Adding to this the report shows negative earnings per share of $1.58. Despite the losses, management is forecasting positive adjusted EBITDA for Q4. The results also showed an improvement in the EBITDA margin from 2019 and 2020, as it improved from -15.6% to -2.7% respectively. Furthermore, the number of outstanding shares kept on growing reaching 344,185,603 from the 340,272,047 representing a dilution of over 1.1%.

Competitors

Given the importance of the Chinese luxury goods consumer, we shall take a look at the competition Farfetch will face in this tough market. JD.com stands as the biggest competitor, given the size of its platform and the number of sales. JD.com, which was once Farfetch’s partner in China, has since been relegated. Both companies reached an agreement in 2017, aiming to conquer the Chinese luxury goods market. Since then both companies have parted ways, and JD.com will definitely be a player and a fierce competitor to Farfetch in the space. Despite the joint venture, Alibaba is a big retailer in the online space in China and could compete indirectly with Farfetch. It should also be noted that Richemont has also invested in the space, with the acquisition of YOOX Net-A-Porter Group.

Secoo (NASDAQGS: SECO) is another company in the luxury goods space. The company has been able to grow at a fast pace, and in 2019 it had revenues of nearly $1 billion. Shanghai-based Meici, which has been in operation since 2008 is a much smaller competitor that still deserves some attention, given that its website receives over 200,000 visitors a month. The company also has a physical location “Meici Cafe”, located in the Mandarin Oriental Hotel in Shanghai. Launched in 2009, 5lux.com is also a big player in the space. The company has sales of over ¥500 million. Xiu.com partnered with eBay (NASDAQ: EBAY), launching ebay.xiu.com, in which Xiu is responsible for handling all sales, logistics, and customer service. At the time of this writing Meici, 5lux, and Xiu remain private companies.

| Farfetch | Secoo | JD.com | Alibaba | |

| Price/Earnings | not applicable | 14.45 | 38.61 | 36.5 |

| Forward Price/Earnings | N/A | N/A | 37.17 | 27.62 |

| Price/Book | 19.06 | 0.56 | 6.27 | 5.57 |

| Price/Sales | 10.72 | 0.15 | 1.26 | 8.21 |

| Price/Cash Flow | N/A | N/A | 31.15 | 23.58 |

| Debt to Equity | 0.83 | 0.67 | 0.28 | 0.14 |

| Net Margin % | -55.02% | 1.05% | 3.33% | 22.55% |

| Return on Equity % | -82.90% | 3.44% | 21.11% | 18.06% |

| Dividend | N/A | N/A | not applicable | N/A |

| Payout Ratio | not applicable | N/A | not applicable | N/A |

Risks

-

High competition

Due to the high growth in the Chinese market, the new Chinese venture will face a lot of competition from well-established companies. This will in turn reduce margins as the company competes for market share. This can also negatively impact the company as it is not profitable, and increased competition in the Chinese market can delay profitability indefinitely.

-

Lack of Profitability

The lack of profits should be a concern for both current investors and prospective investors. Despite being in operation for over 10 years, Farfetch has earned any profits. This fact does not prevent investors from sending the stock soaring since its IPO. But the reality is that for thoughtful investors looking for long-term investing this should come as a big concern.

-

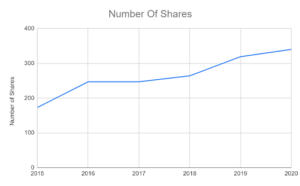

Dilution

Another thing that should keep investors concerned is the dilution in the number of shares that have negatively impacted shareholder value.

Source: Morningstar

Conclusion

Despite the recent agreement, Farfetch remains unprofitable and it is still unclear when it's going to be profitable, or if it will ever happen. The last quarterly reports showed the company lost $0.24 per diluted share. Not only that but the dilution in the number of shares is a terrible sign for investors in the stock. Farftetch seems like a high-risk high-reward stock that you should steer away from. The recent agreement with Richemont and Alibaba, is not so positive for shareholders, as the company will end up giving away part of its Chinese operation that as we have seen will be the one with the highest growth.

The uncertainties surrounding the global economy are a bad sign for the company and the sector it operates in the short term. The European and American markets are both shrinking. Despite the agreement and how it can help Farfetch increase its Chinese exposure, the competition it will face will be fierce. Until a clear path to profitability is shown you should consider other stocks operating in the same space. In conclusion, at this price of over $45, the stock clearly seems overvalued and I would only consider it once EBITDA becomes positive and it shows positive operational signs.

Featured Image Source: FFW

We are long JD. Read our disclosure.