Overview

Mechanical Technologies (soon to be renamed Soluna Holdings) operates two businesses, MTI Instruments and Soluna Computing. Both businesses are profitable and growing at a fast rate, while producing high returns on invested capital. The company was dark and unknown for some time until fund manager Michael Toporek (Founder of Brookstone Partners and CEO of MKTY) took over the company, increased profitability, kick-started growth, and re-emerged MKTY out of darkness in 2018.

MKTY is now listed on the NASDAQ with 12.7 million shares outstanding and a market cap as of writing of $103ml. Toporek currently owns 38.2% of MKTY and has only increased his position in the company since taking control.

MTI Instruments

MTI is engaged in the design, manufacturing, and selling of vibration measurement and system balancing solutions, precision linear displacement sensors, instruments and system solutions, and wafer inspection tools. These products are critical to the manufacturing and inspection of airplanes/aircraft, EV batteries, semiconductor wafers, and plethora of other products.

Most of MTI’s revenue (42.9% as of 2020) is generated from the U.S Air Force. This high customer concentration is slightly concerning, but the Air Force has proven to be willing to continue buying MTI’s products. The products used by the Air Force consist mainly of portable balancing systems (PBS) and precision instrument products. These products are critical to the inspection of aircrafts and related equipment and would be difficult for customers to switch suppliers, therefore I believe MTI will be able to maintain the Air Force as a customer in the coming years.

Since 2020, management has indicated that MTI has experienced significant increased interest for its PBS, diagnostic equipment, and semiconductor products. The new interest has been from EV manufacturers and semiconductor companies. The management has stated that they are actively in communication with such companies and expect the developments of these new market opportunities to accelerate growth.

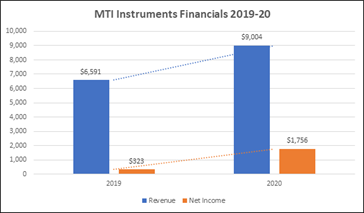

MTI Instruments has been impressive with its growth and profitability over the past few years.

As you can see, revenue grew a healthy 36%, along with net income growing 397%. This is fast growth, which I see continuing in the future. Of course, I don’t expect net income to continue growing at such an eye-popping pace in the coming years.

Based on what the management has been communicating to shareholders, revenue and profitability growth will continue into the long-term. I estimate MTI will grow at a 15% CAGR over the next five years.

MTI seems to be an efficient company with a large addressable market that operates profitably and will be able to grow both profits and revenue over the coming years. Though management has stated MTI will not be a major contributor to earnings in the future, it remains a quality subsidiary. There is also a possibility that management chooses to spin-off MTI into its own stock or sell the business outright to fund the crypto mining operations and its future growth. I do not see this happening soon, but maybe in the future.

Soluna Computing

Before “Soluna Computing” there was EcoChain, Mechanical Technologies crypto mining operation. On August 12th, 2021 the company announced that subsidiary EcoChain was acquiring Soluna Computing. Management further stated that the company will be renaming itself “Soluna Holdings”, along with EcoChain renaming itself “Soluna Computing”. Following the acquisition announcement, management gave an investor presentation laying out the new crypto mining operation and its target goals for the coming years.

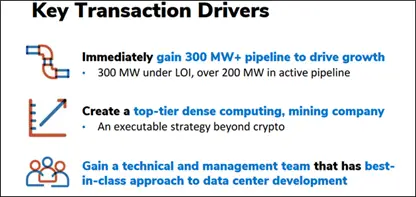

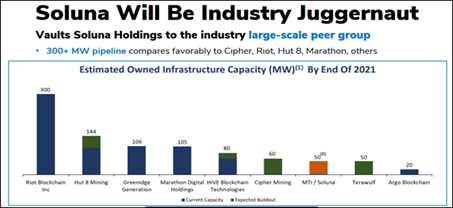

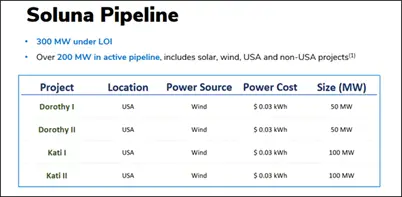

Following the acquisition announcement, management gave an investor presentation laying out the new crypto mining operation and its target goals for the coming years. EcoChain is on target to produce at least 50 MW by the year end 2021. Soluna Computing has a massive pipeline of over 300 MW that will be integrated into the mining operation over the next few years. As the MW are integrated, revenue and earnings will skyrocket.

EcoChain is on target to produce at least 50 MW by the year end 2021. Soluna Computing has a massive pipeline of over 300 MW that will be integrated into the mining operation over the next few years. As the MW are integrated, revenue and earnings will skyrocket.

This acquisition will place Soluna in the top three of mining companies in terms of MW produced. Making them a major player in the crypto mining industry.

The CEO has communicated that the long-term goal is to provide low-cost alternative energy data centers for all things related to blockchain and crypto mining.

Key Advantages

Soluna Computing operates as one of the few 100% environmentally friendly crypto miners. As stated in the company’s presentation, it will generate most of its MW power through wind, along with utilizing natural gas when necessary.

This is an advantage over competitors as companies and governments have expressed concern over the negative effects crypto miners are having on the environment. If Soluna can continue to maintain its eco-friendly image, it will likely become the preferred supplier for many customers.

Although Soluna chose to enter the crypto mining space, they have significant data center infrastructure and advantageous power costs that gives them the ability to pivot to many industries that require computing. I believe this is management’s long-term intention. A unique strategy the company has been implementing is building data centers used to purchase excess renewable energy. This is a smart strategy that provides enhanced power infrastructure and operational flexibility.

A unique strategy the company has been implementing is building data centers used to purchase excess renewable energy. This is a smart strategy that provides enhanced power infrastructure and operational flexibility.

Most importantly, Soluna also holds another intrinsic advantage over competitors...power cost. Compared to other miners, Soluna is the best in class. Below are the power costs of each company broken down:

Riot Blockchain - $0.025-$0.05 depending on location.

Hut 8 - $0.028 via $25ml paydown with supplier.

Bitfarms - $0.022-$0.04 depending on location.

Marathon - $0.028 via equity deal with Beowulf Energy

Digihost - $0.038

Soluna - $0.023

The future is profitability

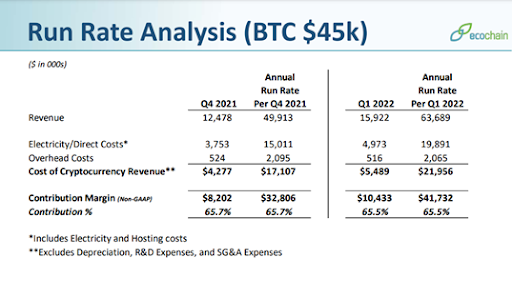

By the end of 2021, Soluna is on track to hit its target of 50 MW produced. In the company’s presentation, it lays out how much revenue and profit Soluna would generate in a full year assuming 52 MW produced and a bitcoin price of $45k:

I estimate that Soluna will be able to produce at least $500k in EBITDA per MW produced. Management has indicated that Soluna should be able to produce between $654k-$834k per MW in contributing margin (their version of gross margin). Soluna spends a negligible amount on R&D expenses, and I estimate a yearly $2ml-$3ml will be spent on SG&A. Given what we know, it seems that most of the contributing margin will result in EBITDA.

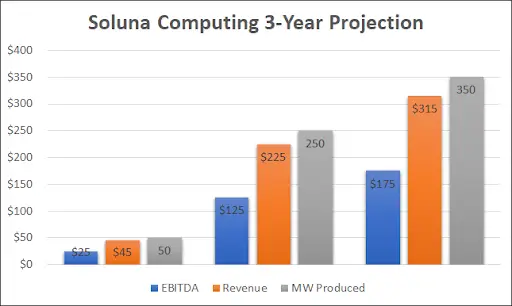

What can we estimate earnings power to be over the next three years? As stated, management says the company will reach 50 MW by year end 2021. By year end 2022, management estimates that they will reach 250 MW. Considering their pipeline and future earnings power, I estimate that they will reach at least 350 MW by year end 2023. Although Soluna has shown that they can produce closer to $800k in EBITDA per MW, I will be very conservative and use $500k per MW in the estimates below:

In a full year of at least 50 MW, Soluna will produce at least $25ml in EBITDA. A full year of 250 MW should produce at least $125ml in EBITDA. This is massive growth in just a few years, but it is very attainable. Management has stated that they have “set the groundwork to achieve our target goals for EcoChain”, using various methods to increase cash equivalents without heavy dilution, including a recent preferred share issuance.

In a full year of at least 50 MW, Soluna will produce at least $25ml in EBITDA. A full year of 250 MW should produce at least $125ml in EBITDA. This is massive growth in just a few years, but it is very attainable. Management has stated that they have “set the groundwork to achieve our target goals for EcoChain”, using various methods to increase cash equivalents without heavy dilution, including a recent preferred share issuance.

Clearly there is massive upside as earnings growth and revenue growth explodes in the coming three years. However, does management have the skill and capital discipline to carry out the plan?

Quality Management

There are many experienced board members and executives at Soluna and MTI, but I would like to take a close look at CEO Michael Toporek.

Below are some excerpts from his CEO letter:

- “I would like to bring a new paradigm of increased transparency to the Company”

- “Our intention is to communicate with shareholders regularly on our goals and the Company’s progress in meeting those goals”

- “As significant shareholders, management’s goal is to earn strong returns on investors capital”

- “We also set the groundwork to achieve our target goal for EcoChain for 2021”

- Toporek stated that they want to be “The AWS for blockchain”.

As stated earlier, Toporek owns 38% of the company, so any dilution or stock price decline would affect him the most. As of 2020, Toporek takes a salary of $25k, including option grants. This is undoubtedly low and sends a strong message to shareholders that he’s not milking the company for his own profit. It also tells me that he thinks the long-term appreciation from his shares will be much higher than any salary or compensation package they could give him.

Finally, Toporek has made good on his word. Since 2016, he has used capital discipline to turn the company profitable and create a valuable crypto mining subsidiary. His capital allocation, transparency, and communication are truly unmatched in the industry.

The rest of the management shares his views on capital discipline and maintaining a high return on invested capital (ROIC) for all ventures. Almost every shareholder call, the term ROIC is consistently used by the COO, CFO and CEO. It is very refreshing to see management that are focussed on being quality capital allocators.

Risks

I see a few risks that could slow the company’s growth or earnings power in the future.

- Brookstone Partners could take advantage of the company due to their majority equity stake. Although this is in the realm of possibility, it is extremely unlikely. If management accomplishes their goals, the company will become very valuable, and Brookstone would profit more than anyone. I believe there is a strong alignment of interest between shareholders and management that would prevent such a risk from taking place.

- MKTY is connected to the cryptocurrency markets, including the price of Bitcoin. This connection can bring more volatility to the stock depending on the price movement of Bitcoin and other such crypto currencies. Soluna is not directly connected to the price of Bitcoin in terms of investment profits or losses because they convert all their Bitcoin to dollars on a daily basis, therefore they do not hold any crypto on their balance sheet (unlike Riot Blockchain and other miners). In the past, MKTY’s stock price has not been seriously affected by Bitcoin falling or rising, thus this risk is likely alleviated.

- A crypto market collapse. This is an extremely low possibility, but in the event of a crypto market collapse due to certain regulation or government intervention, MKTY’s stock would likely take an initial hit. Management has addressed this issue with the conclusion that as long as the company produces power, they can flip to any industry that is involved with computing that requires data center space. So long as they keep producing power at a low price, this risk is minimized and they will always have a pivot option.

Valuation

Thanks to the information management provided regarding their crypto mining operations and MTI business, a reasonable estimate of value can be achieved. My valuation will be based on what I believe the company can do in the near future.

Mechanical Technologies currently has $12ml in cash, and recently completed a preferred stock issuance which provided an additional $18ml. Overall, I estimate the company’s cash position to be around $30ml currently. I believe most if not all those funds will go to upgrading and buying new equipment for Soluna’s crypto operations. These purchases are necessary to the growth of Soluna and will benefit the company in the long-term.

Because the company has not yet started to incorporate the full Soluna Pipeline, I will base my valuation off what Mechanical Technologies will do in a full year assuming Soluna Holdings will conservatively produce at least 50 MW:

Mechanical Technologies Full Year Valuation assuming Soluna at 50 MW:

Revenue - $65ml

Net Income - $26ml

Less: Maintenance CapEx of $5ml.

Free Cash - $21ml

EPS - $2.05

P/E ratio - 15x

Estimated stock price - $30.70

Upside to current price - 377%

Not including the future earnings from the increase in MW throughout 2022-23 and assuming Soluna will produce at least 50 MW in a full year going forward, the stock is significantly undervalued. Additionally, considering that MW produced will be 5x-6x higher in a few years as they fully incorporate Soluna’s Pipeline, earnings will grow exponentially, giving MKTY the ability to be a massive multi-bagger within five years.

Catalysts

Below are the potential events/catalysts that could have a positive effect on the stock price:

- Quarterly earnings. As the crypto mining subsidiary grows, the revenue and earnings growth will start to show up in the quarterly reports. This is the biggest catalyst that will most likely propel the stock higher in the coming years.

- New name/ticker. The company will change its name and ticker after the Soluna acquisition closes in late October. I believe changing the name from Mechanical Technologies to Soluna Holdings could drive more coverage from investors and funds that could potentially affect the stock price.

- Mergers/Acquisitions. I believe management is open to merging or acquiring a smaller crypto miner or related companies. I don’t see this strategy as a key growth driver for the long-term, but it is a possibility, and any such actions could prove to be a catalyst for the stock's growth.

Summary

Mechanical Technologies is an appealing investment for many reasons:

- The company has strong environmental and power cost advantages over competitors that will protect the company's margins and growth in the future.

- The company’s earnings and revenue are set to skyrocket as it integrates its newly acquired pipeline of power over the next three years.

- The CEO is aligned with shareholders, encourages transparency and communication, and sets attainable target goals while maintaining a long-term vision for the company.

- If Soluna only produced 50 MW on a yearly basis, which I believe they will, given the earnings growth that would occur, the company is selling for a significant discount.

- Overall, I believe Mechanical Technologies is a quality company with growing and profitable subsidiaries, along with a stellar management team who I believe will execute their plans to the fullest. If the company meets their target goals in the future, they could indeed become the AWS for blockchain.

Author Bio:

Caleb Leal is a private investor and researcher focussed on finding quality companies at undervalued prices. Since the start of his investment career, he has averaged a yearly return of 32%.

Disclosure: Caleb Leal is long MKTY.

Image source: gadgets